Last Updated on July 23, 2026

Life insurance with type 2 diabetes doesn’t have to be a hassle any longer. When working with Diabetes Life Solutions, we’ll work with you to find the life insurance companies who won’t rate you higher for having diabetes type 2. Our mission is to help people secure the best life insurance for diabetes at affordable rates possible.

When working with us, we’ll take you through the entire application process from start to finish. We promise to make the life insurance application process simple for those with Type 2 Diabetes. This involves us identifying the best life insurance companies for Type 2 Diabetes health profile, as well as making suitable recommendations as to the right amount of coverage you’ll need to secure.

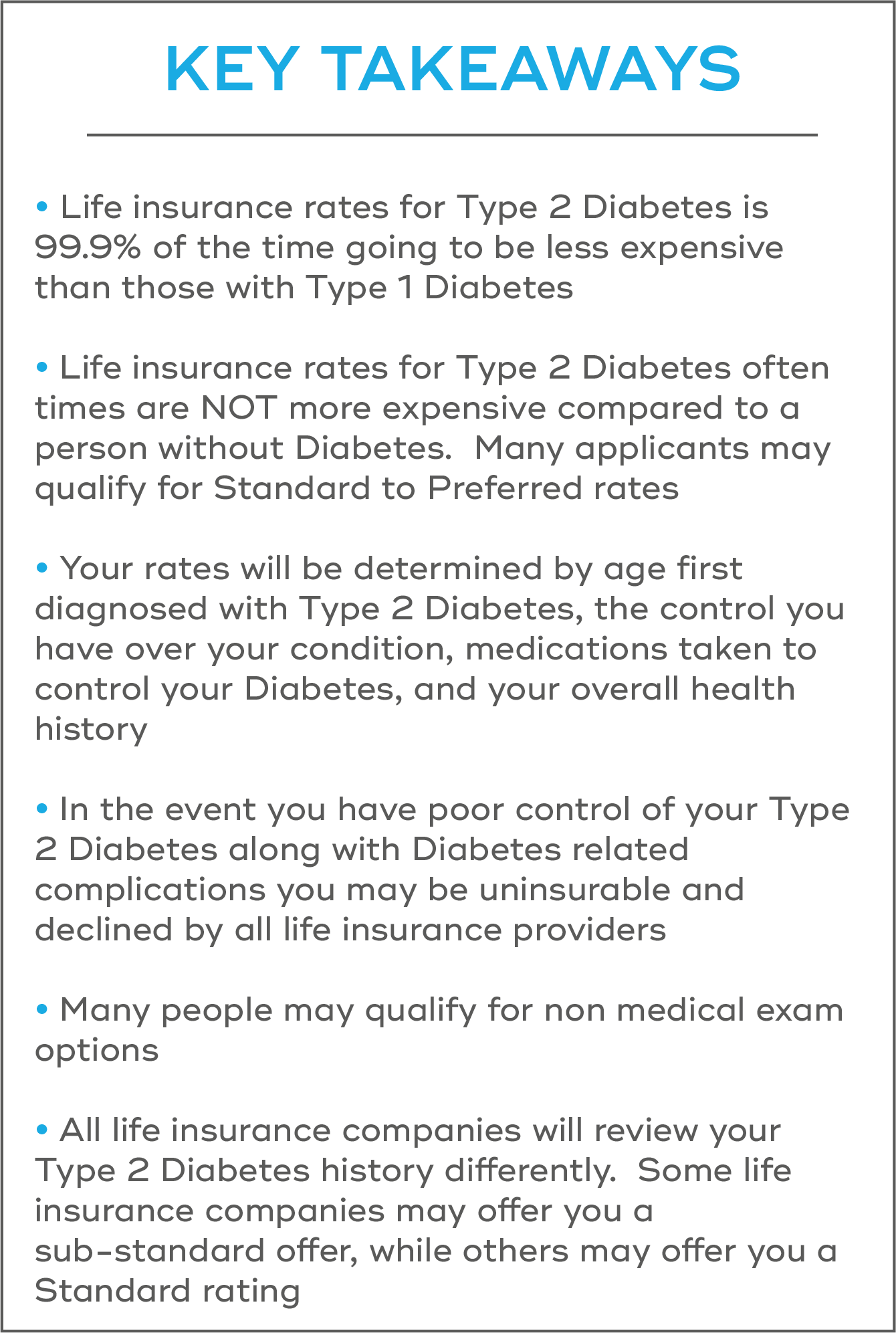

Having Type 2 Diabetes is more common than you think. As of 2020, there are over 30 million people ( Nearly 9% of population) in the United States alone, with this chronic illness. We know that having Type 2 Diabetes isn’t a death sentence, and that diabetics can live a healthy lifestyle. Unfortunately, you may have heard that life insurance for Type 2 Diabetics isn’t obtainable, or affordable. That simply is not true!!!

Life insurance companies are finally understanding that people who have type 2 diabetes often times have the same level of ‘risk’, as non diabetics. Since nearly 1.4 million people every year, are being diagnosed with type 2 diabetes, insurance carriers are making the life insurance process much easier, for this growing demographic. Companies want the diabetes community to be aware that they do in fact have life insurance for diabetes options available to them.

Finding life insurance with type 2 diabetes has never been easier, or cheaper. Rates for people with diabetes type 2 life insurance are at all time lows. Type 2 diabetics also will have a plethora of choices when it comes to choosing from no medical exam policies, as well as lower priced fully underwritten policies. Many people who have type 2 diabetes can obtain life insurance policies that provide living benefit riders, at no additional cost.

However, when it comes to obtaining life insurance with Type 2 Diabetes, it can be a little tricky, navigating the diabetes life insurance market place. It should come as no surprise that life insurance carriers may view you as a higher risk. But what if we told you, that you may not pay higher premiums, compared to people who do not have a form of Diabetes? Chances are, you’ll qualify for life insurance coverage, at a lot more affordable rates then you originally thought. You’ll also have more options, compared to people who are living with Type 1 Diabetes.

Getting Life Insurance With Type 2 Diabetes

Purchasing life insurance is one of the most important purchases that you’ll ever make for your loved ones. It’s the best safety net that you can buy and will give your family the protection that they need, regardless of what happens to you. Or maybe you need life insurance to secure a SBA loan or to meet obligations for a divorce. But if you have Type 2 Diabetes, where do you start to do your research? There’s so much information, and misinformation out on the internet. The best place to start, is by speaking with us.

With life insurance, there are dozens of different factors that the life insurance company is going to consider when you apply for coverage. If you’re a type 2 diabetic, it’s not necessarily harder to obtain coverage, but there may be a few extra steps involved. That’s where an agency such as Diabetes Life Solutions comes into play, as we’ll guide you through the process from start to finish, and guide you to the insurance companies that best suit your needs.

To begin the process of obtaining information for the best life insurance for type 2 diabetics, you’ll need to provide an agent details into your Diabetes history, and overall health. Your health information will allow an agent to share with you various options as to what companies and rates you’ll qualify for.

Good news! Life insurance companies have evolved, and rates for type 2 diabetic life insurance have never been lower! Even better news! There have never been more options to the Type 2 Diabetes community, when it comes to the amount of companies who will offer policies. No longer will life insurance carriers view your Type 2 Diabetes as a death sentence, and charge you outrageous premiums.

To begin the discussion, it’s usually a good idea to let your agent be aware of your needs for life insurance. This will help your agent determine what companies, and what types of life insurance policies that will be suitable, given your financial objectives.

Is it Hard to Get Life Insurance with Type 2 Diabetes?

Quite honestly, it usually isn’t that difficult to qualify for life insurance, with type 2 diabetes. Most people with average, to above average control of their diabetes will be approved by a number of life insurance providers. Diabetes Life Solutions has over a 90% success rate, of getting type 2 diabetes individuals approved for coverage.

Now if you have significant health issues, poor diabetes control, complications from diabetes such as neuropathy or retinopathy, you can expect to have a more difficult time getting approved. As well as paying higher premiums. Some life insurance companies will insure higher ‘risk’ individuals. An experienced agent will be able to help you determine what companies will consider you for life insurance coverage.

Is Life Insurance with Type 2 Diabetes Expensive?

Everyone has a different mindset, as to what they feel is expensive. Many people with type 2 diabetes, will receive an insurance rating of Standard, or better. This simply means that you will not pay higher premiums due to having diabetes.

In our experience, many people think that the life insurance will be expensive initially, and after working with us, feel that the rates were much lower than they initially anticipated. Please keep in mind that the amount of coverage, and type of insurance policy, will have a direct impact on what the premiums will be.

Let’s look at some sample quotes:

Life Insurance Rates for Type 2 Diabetes

$250,000 Level Term Life Insurance [Female – Non Tobacco User]

$250,000 Level Term Life Insurance [Male – Non Tobacco User]

What Do Life Insurance Companies Look At?

Since you have type 2 diabetes, determining your life insurance rates are not as easy as going to an ‘online’ quoter. You’ll need to communicate with an agent, and share with them your diabetes profile. This information will ultimately determine what life insurance rates, you may be eligible for.

In general, the majority of life insurance carriers are going to ask for, and will review the following:

+ Age of your Type 2 Diabetes Onset

The age you were first diagnosed will be a determining factor, for which companies may offer a ‘non-medical exam’ policy. Some life insurance carriers prefer you to be diagnosed with Type 2 Diabetes at age 40 or later. While others may not care what age you were diagnosed, but are just concerned with the level of your control of diabetes.

+ Types of Medications you use to Control Type 2 Diabetes

We know that not every Type 2 Diabetic has the same set of medications, if any medications at all. Life insurance carriers will also vary, in how they rate a person with Type 2 Diabetes, based off their medications.

Some companies may rate you higher, if you take a form of insulin. Other non-medical exam companies, may not offer life insurance, if taking insulin. Don’t worry though, one of our agents can always recommend what companies will still offer no medical exam policies.

If you take oral medications, more than likely you’ll have more options, compared to an individual taking insulin. This varies from individual, to individual.

Ideally, life insurance companies would prefer you to control your Type 2 Diabetes by exercising and dieting. However, not everyone can achieve this. We know that not everyone with diabetes can control their levels, without using medications, and so do life insurance companies.

Our agents will take care of finding the companies which will provide you with the best life insurance for type 2 diabetes.

+ Other Medications

If you are like most people, you probably are being prescribed medication for cholesterol, high blood pressure, maybe even anxiety. Medications like these will have little impact on your best life insurance for type 2 diabetes rates. However, if you are taking a blood thinner, pain medication, or maybe using a CPAP machine for sleep apnea, this may restrict certain life insurance companies from offering coverage. Or depending on complete medical history, extra premiums may be accessed to your policy.

+ Your Height and Weight

As you’re probably aware, your height and weight will be one, of many determining factors for coverage. Fortunately, life insurance companies all have different guidelines. If one company may rate you higher due to height and weight, another company may be able to accept you, at no additional cost. When working with Diabetes Life Solutions, our agents will help make the process simple for you, and will tell you what carriers are ideal for your situation.

+ Tobacco Usage

As you’re probably aware, your height and weight will be one, of many determining factors for coverage. Fortunately, life insurance companies all have different guidelines. If one company may rate you higher due to height and weight, another company may be able to accept you, at no additional cost. When working with Diabetes Life Solutions, our agents will help make the process simple for you, and will tell you what carriers are ideal for your situation.

+ Tobacco Usage

Using tobacco will generally lead to higher rates on life insurance with type 2 diabetes. Possibly 30% higher compared to a non-tobacco user. Not only that, but it may disqualify you from certain non-medical exam policies. If you only use chewing tobacco, a couple of companies will offer NON Smoker rates to you. When you begin your search for information on Type 2 Diabetes Life Insurance, make sure you provide details of your nicotine use to your agent.

+ Control of your Diabetes

People with Type 2 Diabetes, oftentimes have varying degrees of control. This includes your A1C reading, complications of Diabetes and Glucose levels. Like we’ve mentioned previously, all life insurance carriers will look at your control differently.

If you don’t have any significant health issues, and your A1C is ideal, you’ll have no issues getting approved by the majority of companies. However, if your A1C is trending high, your options could be limited. One misconception that Type 2 Diabetics have is that your A1C has to be 7.0 or lower, to qualify for the best rates. This is not true. Companies that we work with look at your entire health profile. If you have an A1C up to let’s say 8.5, you could still qualify for Standard rates with certain diabetic life insurance carriers.

People who have forms of Diabetes complications will have a little trickier time finding coverage. Not all companies will accept the best life insurance for type 2 diabetics coverage if they have complications stemming from the Diabetes. Most likely, you’ll still have options. Simply visit with one of our agents, share your health profile, and we’ll be able to provide some real and accurate information. Depending on the severity of your diabetes complication, you may even be eligible for no medical exam policies.

In general, if you are compliant with your Endocrinologist or doctor’s instructions, you’ll have plenty of options for life insurance. Companies want to be sure that you are taking medications, as instructed, and following up with Dr.’s regularly. Everyone’s body is different, and you could do everything you are told, and your A1C may not dip below 8.0. It’s not the end of the world, as we would recommend companies, who would offer the best rates to you. Everyone’s diabetes, and health profile, is different. Because of this, it’s important to speak with us, so we can help determine what options you would have. Don’t let looking into Type 2 Diabetic life insurance frustrate you! Let the experts work on your behalf, and make the process easy!!!

+ Any Other Health Issues

In addition to your diabetes history, life insurance companies are going to want to know more, about your overall health. Type 2 Diabetes is just one small piece, of your health profile. When applying for life insurance with Type 2 Diabetes, companies will ask about the following:

– Any history of cancer?

– Any history of heart attacks, strokes, or TIA?

– Any kidney, liver, lung disorders?

– Have you been diagnosed with HIV/AIDS?

– Ever been treated for Sleep Apnea?

– Any type of mental disorder?

– Are there any surgeries or procedures that have been recommended, and not completed?

What Types of Life Insurance Policies are Available With Type 2 Diabetes?

If you are living with Type 2 Diabetes, it is quite possible to qualify for all types of life insurance products. Life insurance is broken into two main categories. Term life insurance, and permanent life insurance.

+ Term Life Insurance for Type 2 Diabetics

According to Investopedia term life insurance is defined as “a type of life insurance policy that provides coverage for a certain period of time, or a specified “term” of years. If the insured dies during the time period specified in the policy and the policy is active, or in force, then a death benefit will be paid.” Majority of term life insurance policies provide level premiums, and a guaranteed death benefit, for the duration of the policy.

Term life insurance for people with Diabetes is ideal for people who only need life insurance, for a predetermined amount of time. Oftentimes, due to the lower prices term insurance provides, it may be the most affordable product for you. Over time, as your life and finances change, you can take out additional policies, if needed. Most importantly if you feel you don’t need the policy, you could simply cancel the coverage, at any point in time.

+ Permanent Life Insurance for Type 2 Diabetics

Permanent life insurance is designed to pay a death benefit to the policies beneficiary, no matter the time of death. Theoretically, the policy could pay a death benefit if a person lives to be 60, 85, or 120. If your health changes negatively during life of the policy, you don’t have to worry about being canceled or dropped from the policies.

People with Type 2 Diabetes, generally would have no issues qualifying for these types of policies. One thing we want to point out, is permanent life insurance will be more expensive, compared to term life insurance.

With permanent life insurance you’d have choices of different products, which may help you achieve your financial goals. Some policies are designed to mainly provide a permanent death benefit. Policies like these are known as burial insurance policies. If a person is in poor overall health, they’d need to consider a guaranteed issue policy. These whole life insurance policies will accept anyone, as there are NO health questions to qualify.

Three of the most popular types of life insurance products that Type 2 Diabetics search out for are the following:

Guaranteed Universal Life –These types of policies are great for the person who simply wants a defined death benefit, that covers your life or to certain ages. Most companies will let you choose coverage thru age 80, 85, 90,100,110, or 121. Guaranteed Universal Life doesn’t put a focus on cash value, and is designed again, to provide a specific death benefit, with guaranteed level premiums. If you have Type 2 Diabetes, you’d have a plethora of choices, for life insurance carriers.

Indexed Universal Life –For some people, this type of life insurance offers what they consider the ‘best of both worlds’. Meaning that in addition to providing a permanent death benefit, the policy would accrue cash value as well. Your cash value would be indexed to indexes such as the Nasdaq 100, or S&P 500. Over time, there would be strategies that you could utilize, to access this cash value. Many people even ear mark this type of policy, as an asset, for their retirement.

Whole Life Insurance –Whole life insurance is one of the most well-known types of coverage. Whole life insurance provides a guaranteed death benefit, which means that your beneficiary receives a lump sum, tax free benefit at time of your death. These policies build cash value over time. Unlike Indexed Universal Life policies, the cash value is not ‘tied’ to the stock market. But rather the various life insurance carriers pay out ‘dividends’ annually. The dividends can be applied to your cash value, or even be used to help pay premiums.

Do you have to Take a Medical Exam to Qualify for Coverage?

In most cases, if you prefer to not complete a paramedical exam, you would have no medical exam life insurance options. To determine what options you would have, you simply need to speak with us, and share with us the particulars to your type 2 diabetes history.

To qualify for a no medical exam policy, you’ll have to answer basic health history questions, and details to your type 2 diabetes. In addition to the information you provide on the application, companies will do a prescription drug background report. All information gathered will determine your eligibility.

What is the Application Process for Life Insurance?

The life insurance application process is pretty straight forward. All life insurance companies are going to require you to complete a basic application. You will need to share your personal information, beneficiary information, employment information, and basic financial information. The type of information that is collected is standard across the board.

If applying for a fully underwritten policy, the next step will be to schedule the medical exam. This 20 minute examination consists of a nurse visiting you at your house or place of business. In addition to asking you basic health questions, they’ll collect a blood and urine sample.

While you are waiting to complete the examination, your agent will also order the necessary medical records, that companies will need to review. Generally this is the last 5 years worth of diabetes medical records. The information in your medical records, and the lab results, will be used by the insurance companies to determine your final rates.

If applying for a no medical exam policy, the process is the same, except for the examination and medical records. The only other step that may be required is a phone verification interview.

How to Get the Best Life Insurance Rates for Type 2 Diabetics

One of the most common reasons that people don’t purchase life insurance is because they assume that it’s going to be too expensive to fit in their budget. In most cases, this couldn’t be further from the truth. There are plenty of ways that you can get an affordable Type 2 Diabetes life insurance policy.

As discussed, the various life insurance companies are all going to view your health profile differently. The first thing to do is to speak with one of our agents, or fill out an online quote request. From there, there may be a couple of things you can do, to improve your rates. Here are some tips, to help you secure the best possible life insurance rates, with type 2 diabetes.

+ Health Improvements

One thing you can do, is do a quick inventory of your overall health. Before applying, maybe you could lose a few pounds. Perhaps, by losing 5 pounds, you would qualify for a better premium. This is always a good idea especially if you are applying for a policy that requires a mini-physical exam.

Or maybe you’re thinking of starting an exercise regimen. We know of a life insurance company that rewards Type 2 Diabetics, who exercise regularly. Showing a life insurance company that you are living a healthy lifestyle, will only improve your life insurance premiums. Not to mention, that exercising helps with your diabetes control.

+ See an Endocrinologist

Not everyone sees an endocrinologist, but studies have shown that individuals who do, tend to have better control of their Diabetes, and overall health. Life insurance companies have picked up on this. As a matter of fact, we know a couple of select companies, who will provide discounted rates, for Type 2 Diabetics who have a great overall health profile, and see an Endocrinologist 3-4 times annually.

Another recommendation is to apply for life insurance, shortly after seeing your medical professional. Like most Type 2 diabetics, after your Doctor appointment, you’ll receive results from your blood work. You now have a great idea, as to where you vital levels are at. If they are favorable, it may be a great time to begin applying for coverage. That way, there won’t be any surprises when it comes to the blood and urine test.

+ Stop Using Tobacco Products

The next thing that you should do is eliminate any tobacco that you currently use. Like we previously mentioned companies may increase your rates by 30% or higher. Life insurance companies will want you to be tobacco free for up 12 months or longer, to consider for non-tobacco rates. (If you are a tobacco chewer a couple of companies will offer nonsmoker rates)

We know life insurance is important, so it may not be wise to wait one year for coverage. If you take out a policy with a tobacco user rating, you can apply in the future. Perhaps saving money on life insurance is motivation, to kick the habit.

+ Use Technology

Many of us like to use Fitbit, and other health related technology. What you may not know, is that multiple life insurance carriers may offer discounts on life insurance for Type 2 Diabetics. If you allow insurance carriers to monitor your daily activities, you can save money on your life insurance premiums. The discounts may seem small at first, but over time, they can be significant.

Work with An Independent Agent

When applying for life insurance, irregardless if you have type 2 diabetes or not, you’ll want to work with an independent life insurance agent. Working with an agent, who represents multiple life insurance companies, will generally be your best bet when applying for life insurance with diabetes. Being able to run your health profile past multiple companies will help you determine what carrier, will be the most competitive.

Working with Diabetes Life Solutions, we promise to put your needs ahead of our own. Simply meaning we work for you!! And not any one particular life insurance company. Our only job is to help you find the best priced life insurance policy, given your health profile.

A lot goes into the life insurance application process. Don’t feel overwhelmed! We are here to help. A quick phone call into our agency will help you get pointed in the right direction. Our agents will discuss with you what plans, and companies, that will be ideal for your given health profile. Let us use our expertise to help you secure the best priced policy possible.

No Medical Exam Life Insurance Policies for Type 2 Diabetics

One option for getting Type 2 Diabetes life insurance coverage is to purchase a no medical exam life insurance policy. As you can imagine from the name, these plans give your life insurance coverage without being required to take the medical exam first. Most life insurance providers will simply have you answer basic health questions, do a prescription background check, and also do a Medical Information Bureau review. Some companies may order your most recent medical records. Don’t want to do exam, nor want your medical records reviewed? No problem. You should have options available to you.

If everything checks out on your background review, you may receive a decision in a matter of minutes, or days. These non-medical exam policies are great for people who need coverage to settle a divorce decree, or maybe to cover a SBA loan. You can get the coverage you need in a timely manner, as opposed to waiting weeks or months.

Type 2 Diabetics would have non-medical exam term life insurance and whole life insurance options available. Or if maybe just needing a burial insurance policy, you can quickly obtain one of these, to address final expenses. Again, no medical exam would be needed.

These plans are also a great option for a lot of diabetics that don’t have their condition managed well. As a type 2 diabetic, your glucose levels and treatments are going to play a huge role in how much you have to pay for your policy. Some non-medical exam policies don’t require you to have an ideal A1C, but rather you just not having any major diabetic complications. Potentially a no medical exam life insurance policy would be less expensive, compared to a policy that tests your A1C.

If you don’t feel like your Diabetes control is up to par, it could be a good idea to initially take out a policy that doesn’t require a medical exam. In the future, if your diabetes control does improve, you can always re-apply for a policy that requires this additional testing.

While these plans are a great way for anyone to get life insurance protection, they may be more expensive than a policy that requires a medical exam. If looking for the ‘lowest’ rates possible, visit with us, and we will let you know if you’re better off going thru a policy, that requires an exam. Life insurance for Type 2 Diabetics is attainable, and it’s possible, a non-medical exam policy is your only choice.

You can’t put a price tag on the peace of mind a type 2 diabetes life insurance plan will get you, but these no exam policies could be the best type of plan for you.

Work With Independent Insurance Agents

The best way to get the lowest insurance rates (in this case for type 2 diabetic life insurance) to work with one of our independent insurance agents. Unlike a traditional insurance agent, our independent agents work with dozens of highly rated companies across the nation. We can help you find the best plan to meet your needs and provide you with the information that you need. If you feel like shopping around to all the different life insurance companies is a task that will take weeks of your time – you’re right, it probably will. This is why we work directly with people with Diabetes to help them shop. Let us do all of the hard work!

In this industry, the word “agent” isn’t a bad word – they can usually help you get a cheaper rate than you would be able to secure on your own. The best part is, they can take down your information and shop it around to the companies they know will be offering decent rates for your individual situation. Even before beginning the application process, a knowledgeable agent can help obtain tentative offers, from various companies.

Applying For Life Insurance Doesn’t Have To Be Complicated

So even though the process of applying for Diabetes life insurance is something that makes Type 2 diabetics really wish they didn’t have diabetes, it doesn’t have to be so bad. Just remember to make sure you work with agents who have an understanding of the Diabetes community.

Your family and their future are too important to continuing going through life uninsured – explore your options today. Diabetes Life Solutions was founded by people with Diabetes, that wanted to provide the Diabetes community a better way, of going about applying for life insurance.

The application process has been simplified by us, and we promise it will not be a lot of work. An application takes about 10 minutes to complete, and from there, our team handles everything else.

If you have any questions about getting life insurance for people with type 2 diabetes, please contact one of our qualified agents today. We would be happy to answer those questions and ensure that you’ve got the best plan to meet your needs.

Our agents have years of experience working with diabetic applicants and we know which companies and plans are going to get your family the best protection at an affordable rate. Don’t feel like the life insurance application process has to be difficult. We make everything as easy as possible for our clients.

You never know what’s going to happen tomorrow, which means that you shouldn’t wait any longer to get the life insurance for diabetics type 2 that you or your family deserves. If something tragic were to happen to you, and you didn’t have life insurance, your family could be left with a massive hole of debt and no money to cover those expenses.

Being left with thousands of dollars debt is going to make an already difficult situation a thousand times worse. Making the right decision by getting diabetes type 2 life insurance can and will change your life. Contact us or request your free life insurance quote today! We promise to make your application process as simple as possible, and we’ll provide the highest level of customer service possible.