![]()

![]()

![]()

Last Updated on August 4, 2026

Divorces are rarely ever wonderful. And, why would they be? They are the finalized product of a love-went-wrong. Most people want to get over it and move on as quick as possible. For some, without any kids or accounting nightmares, that may be possible. However, for others, not so much.

There is a lot to be considered in a divorce – especially when it means separating a family. It takes time to sort through finances, assets, property, and such. Dissolving the marriage – a life together – is no easy feat. So, while the details are being worked out, there are a few things that you’ll probably have questions about. One of those questions is likely to do with life insurance. Life insurance and divorce are major points of discussion. Questions like what happens to life insurance in divorce constantly revolve in our mind.

As a couple, you had life insurance for one another. And, you likely put each other as the beneficiary since, after all, who knows you better than your own spouse, right?

But, as a divorcing couple, what do you do? Do you keep the policy? When do you let it go? Should you change the beneficiary? Are you even allowed to do that? What steps should you be taking with regard to the insurance policy now and for the future? Life insurance in divorce settlement play an important role.

Lots of questions will be going thru your mind, that is for sure. Here are some tips for you.

Confirm Your Ownership Rights

First and foremost, you will want to confirm your ownership rights. If life insurance policies were purchased during your marriage, you may have a policy on your ex-spouse (or soon-to-be) and vice versa.

Perhaps you’d like to continue with that existing policy, but you need to make some adjustments. If you are not listed as the policy owner there is nothing you can do. Your first step of action should be to determine who is listed as the policy owner. A quick call to your agent or insurance company is all that it takes.

Only the policy owner can make changes to the policy. If your ex-spouse has a policy on you that was purchased before you got divorced, you likely signed something giving him or her authority to do so. To have your ex removed, you will need to talk with your insurance company and have some documents signed turning ownership over to you. During life insurance and divorce, your attorney can work with your ex-spouses legal counsel to get this done. Or if the divorce is amicable, hopefully you’d be able to make these changes without having to spend money on attorneys.

Changing Your Beneficiary

The beneficiary is the person who would receive the payout on a life insurance policy upon the death of the insured. Typically, if you have a life insurance policy on yourself, your beneficiary is likely your spouse. Again, it is incredibly important to check the ownership and take the necessary steps to move the ownership rights into your name. This is the only way to change the name of the person listed as the beneficiary. Contact your agent, or your life insurance company, and ask them to provide a ‘change of beneficiary’ form. This simple form takes five minutes to complete, and you can make sure your policy’s beneficiary is correct, and accurate.

Note: There are two different types of beneficiaries – revocable and irrevocable. The only one that allows you to ever change your beneficiary is a revocable policy. Generally, when taking out a life insurance policy, you’ll want to have beneficiaries be revocable. It’s impossible to predict the future, so having the ability to change a beneficiary is usually in your best interest.

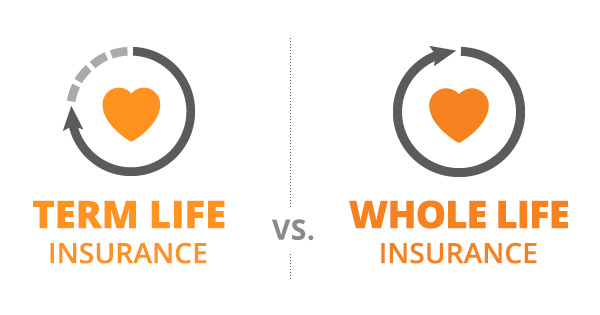

Life Insurance Cash Value Should Be Considered

During divorce proceedings, there is a lot of paperwork you have to fill out – and a lot of financial information you need to provide. Depending on the type of life insurance you have, you may be able to use the cash value as an asset and identify each part of life insurance cash value in divorce.

Term life insurance has no cash value and doesn’t build up anything over time. On the contrary, whole life insurance, indexed universal life insurance and variable life insurance build up a cash value over time. When your monthly premium is made, a percentage of this is paid to the policy and another percentage is paid to a fund that grows with interest. At any time that the policy is active, you can elect to forego the death payout and cash out your plan.

This money can be considered an asset of the marriage and should be addressed in the divorce proceedings. If you decide to surrender the policy, and to divide the cash value, the life insurance policy will not be enforce. The life insurance cash value in divorce is much more than you an expect. Most companies simply require a ‘surrender form’ to be completed, to cancel the policy. The cash value would then be paid in a lump sum payment, to the policy owner. And this is how life insurance and divorce proceed smoothly.

Protecting Your Children

Take into consideration that divorce, often times ends in someone becoming a single parent. With no other parental figure in the picture to take care of your children when you die, you need to make some plans.

Your children will be overcome with grief should something happen to you. Not to mention that if you are their sole provider, they will be left with nothing. A guardian, such as a relative or a representative of the state will take on the responsibility of your children. But with so many unknowns, you want to make sure they are left with something. Make arrangements now so this cannot happen.

Your children will be overcome with grief should something happen to you. Not to mention that if you are their sole provider, they will be left with nothing. A guardian, such as a relative or a representative of the state will take on the responsibility of your children. But with so many unknowns, you want to make sure they are left with something. Make arrangements now so this cannot happen.

In the midst of your divorce, get a clear vision of what you need to do to protect yourself and your kids. And one thing you must do is obtain life insurance. Do so in a way that you know that your children will be provided with their basic needs and then some should you not be able to. Even consider college. Applying for a new policy would be easier than you think, even though you have Diabetes. Simply contact an agency, such as Diabetes Life Solutions, to have them help you find a diabetes life insurance policy.

It may be overwhelming to determine the amount of coverage you will need, but here is a simple formula: multiply your annual salary by how many years you have until your youngest child turns 18 or 21. That is the minimum amount of life insurance coverage you will need. Or if the court has ordered an exact amount needed, we can help you obtain this coverage.

Looking Out for Child Support & Alimony Income

Do you have primary custody of your children? Do you receive income from your ex-spouse that you rely on? What would happen to you – or you and your children – should your ex-spouse die?

Do you have primary custody of your children? Do you receive income from your ex-spouse that you rely on? What would happen to you – or you and your children – should your ex-spouse die?

You need to have something in place to supplement this income should something happen.

Child support and alimony income are only received if the ex-spouse is alive to give it. Consider purchasing a life insurance policy on your ex-spouse for an amount that would continue to let you live comfortably. Often times, this can be negotiated as a part of the divorce settlement.

Court Ordered Life Insurance Obligations

Often times, to complete your divorce, you may be ordered to obtain a life insurance policy, and show proof to the courts. Having diabetes, you do NOT want to wait until the very last second, to obtain this coverage. Depending on if you have Type 1 Diabetes or Type 2 Diabetes, you may only qualify for a policy that requires blood and urine testing, as well as a review of medical records. The whole process may take up to 30 days for an approval. Courts don’t like you not being proactive, and not having the life insurance in place, before their deadlines. Be particular about your court ordered life insurance.

If you medically qualify, and only have limited time to obtain a policy, you can explore no medical exam life insurance options. Policies like these take a matter of days, for approval. Not everyone will qualify. To find out if you qualify, simply call us at 888-629-3064. In a matter of minutes an agent will share with you your options.

Depending on your situation, your ex may be ordered by the court to obtain and manage the policy on his or her own, leaving you or the children as the beneficiaries. Or, if you want to feel confident, then you may purchase and pay the premium so that you are the policy owner and can rest easy.

Final Thoughts

Just because you are getting divorced doesn’t mean that you necessarily want your lifestyle or financial situation to change. You just want your ex-spouse out of your life. Keep a clear head and don’t make hasty decisions. Ask questions, make sure you are the policyholder of the life insurance in divorce settlement and that you change your beneficiaries upon finalization of your support.

Life insurance can save your situation, whether it is as a backup for child support or alimony, protection for your children, or even for yourself. But with so much going on with the divorce, it is easy to make mistakes.

No matter your situation or need, an insurance agent can help you get what you need. Agents are professionals who know the business inside and out – and have connections to get you just what you are looking for. So, don’t push your life insurance to the back of your divorce file. Get an agent on your side as soon as possible.

Contact us today! We would love to assist you if needing a policy, to fulfill a court order. We can help you understand everything related to what happens to life insurance in divorce. We handle these types of cases all the time, and would be able to help you get the policy you need. Diabetes Life Solutions only works with people who have Diabetes. You will not find another organization, who specializes to the degree that we do.

Contact us today! We would love to assist you if needing a policy, to fulfill a court order. We can help you understand everything related to what happens to life insurance in divorce. We handle these types of cases all the time, and would be able to help you get the policy you need. Diabetes Life Solutions only works with people who have Diabetes. You will not find another organization, who specializes to the degree that we do.