Last Updated on July 4, 2026

Whole life insurance for diabetics is a popular choice of coverage. Many individuals can benefit from a permanent form of life insurance, which also provides cash value growth over time. There are many uses for purchasing the best whole life insurance for diabetes, as it can be a very flexible type of insurance product. Some people like the idea of a policy accumulating cash value, while others would want a whole life policy to address burial costs and end of life expenses.

For whatever reasons, many misconceptions still exist when it comes to diabetes and whole life insurance. People often have queries like can a diabetic get whole life insurance? Yes! You can qualify for whole life insurance if you live with a type of diabetes. Living with diabetes is NOT an automatic reason for a decline in coverage.

Quick Article Guide

Here’s what we’ll cover in this post:

People with Diabetes Can be Approved for Whole Life Insurance.

If wanting to explore all of your life insurance options, please contact us at 888-629-3064 to speak with a licensed agent. We assure you that having Diabetes will not be an automatic decline of coverage. In order for us to determine what specific life insurance companies may be the best fit for you, we’ll need to know more about your diabetes history and overall health.

Here at Diabetes Life Solutions we only work with the Diabetes community, so we know which life insurance companies will be your best fit. In order to determine this, we’d simply need to know more about your financial objectives and your overall Diabetes history. Whole life insurance is a very valuable form of coverage as it can help cover your final expenses, or the cash value component to the policy may be a part of your retirement portfolio.

People of ages, even children with type 1 diabetes may qualify for whole life insurance coverage. We’ve helped families all across the country obtain affordable whole life insurance for type 1 diabetes. If another agent tells you that you can’t qualify for a policy, don’t be discouraged. Just contact us and we’ll share our honest opinion.

2020 through the present has been an interesting time to say the least. Covid 19 or Coronavirus has made living with Diabetes difficult. This deadly virus has also impacted what types of policies life insurance companies will offer, and who they will offer to. Never before have life insurance companies worried so much about your profession, or about your past or future foreign travel plans. As we all know, living with Diabetes is not easy. And sometimes finding whole life insurance for diabetes can be challenging.

Luckily, almost every life insurance company has reverted back to the same underwriting guidelines that were used pre Covid-19. Because of this, finding whole life insurance with diabetes is easier currently than over the past 24 months. Not to mention, whole life insurance underwriting guidelines tend to be more favorable, compared to term life insurance. Many consumers are not aware of this.

Whole life insurance with Diabetes can still possibly be obtained, and it’s getting easier than in years past. To receive information please call us at 888-629-3064 or fill out a quote request. A licensed agent will be able to work with you, and help determine what life insurance options you will have available to you. In the event you’ve been declined coverage in the past due to Diabetes, do not give up hope. Just contact us.

Can you obtain a whole life insurance for diabetics policy currently? It’s quite possible. But we’ll simply need to know more about your health profile before making any suitable recommendations. Diabetes is impacting nearly 34 million people in the United States alone. Not to mention almost 85 million people having pre-diabetes. This means there is NO ONE BEST life insurance company for diabetics. The best company will vary from consumer to consumer. Having this type of chronic illness makes applying for life insurance more difficult compared to a person living without diabetes. insurance in this current environment tougher than in the past.

What is Whole Life Insurance?

According to New York Life insurance company, “whole life insurance is for those looking for lifetime protection with added benefits. In addition to providing a guaranteed life insurance benefit, it also offers an important way to save for the future, helping you to be prepared for whatever lies ahead. With Whole Life, the cash value of your policy grows tax deferred—which means you can use it whenever you need to, whether for a new home, college tuition, or an income stream in retirement. Dividends provide an opportunity for the cash value to grow more.”

If considering a permanent policy to protect your family, whole life insurance is probably worth taking a look into. In addition to providing a guaranteed death benefit to your named beneficiary, the cash value growth could be an asset for you in the future. This cash value could be borrowed from the policy thru a loan provision.

Image Source: Diabetes 365

Whole Life insurance is an excellent safety net that you can purchase to ensure that your loved ones have the money that they need, regardless of what happens to you. When you’re applying for whole life insurance for type 2 diabetics, there are dozens of different factors that the insurance company is going to look at when reviewing your application that determines your final rates. Your Diabetes history will be one of many determining factors, when a life insurance company reviews your complete health profile.

Here’s a quick breakdown of what most life insurance companies will view in order to determine your final rates of coverage:

- Age at time of applying

- Gender

- Age first diagnosed with Diabetes

- Medications being prescribed for your Diabetes

- Control of your Diabetes

- Complications from Diabetes

- Any other significant health issues not related to Diabetes

Whole Life Insurance for Diabetics is Easily Obtainable

People with Diabetes can often feel like their options are very limited and that protecting their family in the event of something unexpected is not an option. Fortunately though, this is not at all the case and the best whole life insurance for diabetics can definitely be obtained, and much more easily than you might think. We work with over 70 different life insurance companies so we’ll help you determine which provider will be ideal for you and your family.

The main thing to remember when applying for whole life insurance with diabetes, is to always work with a trusted life insurance agency who specializes in diabetes life insurance, like us.

You can ask us all the necessary questions, and can rest assure that we’ll only provide you real and accurate life insurance information. Having Diabetes isn’t a death sentence, but not all life insurance companies will view your health profile the same. One life insurance company may rate you considerably higher, where as another company would offer Standard rates. Obtaining life insurance with Diabetes is easier than you can imagine. You just need to work with an agent who’s properly trained to work with the Diabetes community.

Don’t let this worry you, as this is where we come in to help. We communicate to these companies on behalf of the clients, and will make your health profile look as positively as possible. Just call us at 888-629-3064 and an agent will be more than happy to speak with you. A quick 5 minute call is all that it takes, to share with us your Diabetes and health history.

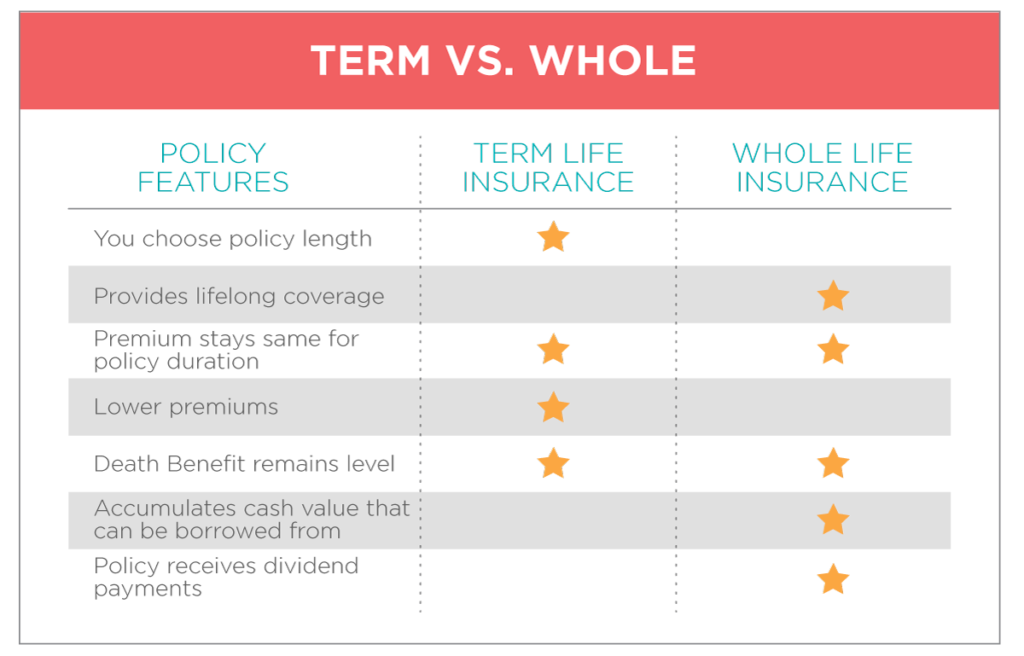

Whole life insurance is one of the most common life insurance products out on the market place today. People with diabetes usually can qualify for these type of plans, without too much effort.

A whole life insurance policy will offer a permanent life insurance product for the insured, assuming premiums are paid to keep the policy in force. These premiums would remain level for the duration of the policy or until you wish to stop paying premiums.

With whole life insurance, the death benefit is usually a specified amount, defined in the policy contract. Most policies will receive dividend payments. The owner of the policy can choose to have dividend purchase additional life insurance coverage, which in turn increases the death benefit over time. Majority of policies also allow for riders that can waive premiums if you become disabled, or even living benefit riders. These types of life insurance riders allow you to access the death benefit, while living if you were diagnosed with a chronic, terminal, or critical illness.

These whole life insurance policies for diabetes also include a cash value account, in addition to the death benefit. This cash value is a savings component that may accumulate interest on a tax-deferred basis. Cash value based policies may be beneficial to you and your family, if seeking a policy that offers more than just a death benefit. Your cash value can be utilized thru a ‘loan’ of the policy, or should you choose to cancel the policy at a future date, the cash value would be paid to the policy owner.

Another important feature of a whole life insurance policy is the Dividend history the company has paid in the past. A participating whole life insurance policy is designed for the policy holder to receive an annual dividend payment. What is a dividend exactly? Investopedia states “Many whole life insurance policies for diabetes provide dividends representing a portion of the insurance company’s profits that are paid to policyholders. In many ways, these dividends are similar to traditional investment dividends that represent a share of a public company’s profit.”

There are many ways an insured could utilize these dividend payments. Investopedia claims these are some of the most common uses of dividends:

- Cash or check: A policyholder may request that the insurer send a check for the dividend amount, which may be subject to dividend taxes.

- Premium deductions: A policyholder may request that the dividend be put towards their future premiums owed in order to offset the cost.

- Additional insurance: A policyholder may use the dividend amount to purchase additional insurance or prepay on their policy.

- Savings account: A policyholder may decide to keep the dividend with the insurance company in order to earn interest on the amount.

Topwholelife.com has done an excellent job of tracking various life insurance companies, and ‘charting’ their dividend history. Here’s a quick look at some popular insurance companies, and their recent dividend payouts.

Credit topwholelife.com

Just like for any other person, applying for the best whole life insurance for diabetics means you will have to go through an underwriting process. This goes for people who have Type 1 Diabetes as well as Type 2 Diabetes. Certain companies will be more friendly to people with Type 1 Diabetes, where others are more favorable to the Type 2 Diabetes Community. This is where we come into play, as we’ll help you navigate the diabetic whole life insurance market place.

When it comes to life insurance, the job of the underwriter is to assess the amount of risk you present to the insurance company by reviewing your health and the severity of your condition. Each whole life insurance company will have specific underwriting guidelines, that will determine your rates, and eligibility. One life insurance company may rate you significantly higher, than another. It may make financial sense to compare costs from various life insurance companies. This is something that we do everyday for our clients.

Obviously, the more severe your diabetes condition is, the more risk will be perceived by the insurance company and the more you will end up paying for your whole life insurance.

At Diabetes Life Solutions we are dedicated to helping you get the best life insurance for diabetics. We work on the behalf of our clients, and work to secure them the best types of policies, based off their financial objectives. Every consumer we work with is different, and what they need in terms of life insurance will vary. We’ll work with you to customize an insurance portfolio that’s suitable for your financial goals.

Whole life insurance is not the cheapest form of life insurance. However, if you want a permanent life insurance policy that accumulates cash value, this type of policy may be a good fit for you. Or if not needing a permanent policy, maybe a term life insurance policy for Diabetics is a better fit. What many people with Diabetes don’t realize is that you will more than likely qualify for the same types of policies for whole life insurance for type 1 diabetics or type 2 as a person who doesn’t have Diabetes. If unsure of which type of policy you are in need of, just contact us. We would love the opportunity to help you determine which type of life insurance will suit you the best.

What is the Application Process?

When applying for life insurance, you’ll need to complete a basic application. This application consists of you providing your personal information, answering health questions, and life style questions. Once you have completed an initial application, your agent can then begin processing.

Life insurance companies will also do a MIB ( Medical Information Bureau) review, as well as a Motor Vehicle Report.

The next step will be for the insured, to complete a paramedical exam. This many physical simply consists of a licensed examiner to take your Height, Weight, Blood and Urine sample. Those labs are then sent off, and results are shared with life insurance companies.

While you are waiting to complete the paramedical examination, your agent will begin ordering the necessary medical records. Most companies are going to want to review the last three to five years worth of medical records.

Once the lab results and medical records are received, a life insurance company would be able to make an actual offer. This offer would determine the exact rates of the whole life insurance policy. Generally, the application process will take three to four weeks to complete.

Your complete Diabetes, and health profile determines the final rates. If labs and medical records are favorable, you may qualify for Standard rates or better. Or if your overall health profile has some ‘red’ flags, you can be declined all together for coverage. For applicants who apply using this fully underwritten method, final rates will not be determined until the underwriting process is completed.

For those individuals who would like to know which companies provide the best whole life insurance for diabetics, simply fill out a quote request. Or contact us. As soon as we have a clearer picture of your diabetes profile and financial objectives, we can help determine specific life insurance providers.

No Medical Exam Whole Life Insurance Plans

If you’re a diabetic, one option to get an affordable whole life insurance policy is to purchase a no medical exam policy, which will give you life insurance without being required to take a medical exam. These types of policies are ideal for people who do not want companies to collect and blood or urine sample, nor review their medical records. If you fall into this category you’d have a wealth of options available to you.

In some situations, a life insurance company will waive the examination, and review the past four to five years of your medical records. The health and Diabetes information in your health profile would determine your eligibility and the final rates for life insurance. It’s our job to help you choose the perfect application process for your situation.

Or specific life insurance policies will NOT review records nor require an examination. They’ll simply do a Medical Information Bureau check, and prescription history review. If nothing negative comes up with these background checks, you’ll be approved.

Because you have diabetes, the insurance company may give you higher rates, or even decline your application for whole life insurance for type 2 diabetes. Again various companies will have underwriting guidelines in place. Depending on your overall health profile, you may NOT pay higher premiums, compared to a person who doesn’t have diabetes. Here are some sample diabetes questions that non-medical exam companies will ask, on their whole life insurance applications:

- Do you have type 1 or type 2 Diabetes?

- If you have type 1 diabetes, how many units of insulin do you take daily, on average?

- What age were you first diagnosed with Diabetes?

- Do you use any type of Diabetes related technology?

- What are your most recent A1C levels?

- Have you ever been diagnosed with having a diabetes related complication?

- What type of medications do you take to control your Diabetes?

- Do you watch what you eat, and have an exercise program?

- Are you seeing an Endocrinologist?

- What is your approximate height and weight?

In addition to asking basic health questions, insurance companies will do a prescription drug background check, and a Medical Information Bureau review. These findings allow them to make a decision. Good news for people who want an IMMEDIATE decision on their application. When applying for a non-medical exam whole life insurance policy, companies will make a decision in 48-72 hours.

There are several advantages and disadvantages that you should consider before purchasing a no medical exam plan.

Advantages

The most obvious benefit to these plans is that almost anyone can purchase life insurance coverage, regardless of health or any pre-existing condition that you have. Everyone should be able to get life insurance coverage, and your health shouldn’t stop you. Even people in poor health, with less than ideal control of their Diabetes, can qualify for burial insurance policies. Usually they would qualify from ages 25-85. These whole life insurance policies for diabetics would approve anyone who has Diabetes, along with any other significant health issues.

Another advantage to these plans is that you can get whole life insurance coverage much quicker than you can with a traditional policy that requires you to take a medical exam. With a normal life insurance plan, you’ll have to wait to schedule the exam, wait for the results, and then wait for the insurance company to review your results. Instead of waiting for approximately 30 days, you can get an approval in a matter of days. Some whole life insurance applications can be approved in a matter of minutes.

Disadvantages

One of the disadvantages of these non-medical exam policies is that they may be much more expensive than a traditional plan that requires a medical exam. The purpose of the exam is to give the company an idea of what your health is, but with a no medical exam, they don’t get that picture of your health. When working with an agency like us, we’ll help you determine which possible policy, is the best for your situation.

Because the insurance carriers don’t know your overall health, they are taking a higher risk to give your life insurance, and they may offset that by giving you higher monthly premiums. If you want the most affordable coverage, you’ll generally want to seek out a policy that requires a medical exam plan. This isn’t always the case though, and is an important reason why you’d want to speak with us beforehand.

For some people, a non medical exam whole life insurance policy will be the perfect fit for them. Oftentimes the non medical exam plans have more lenient underwriting guidelines, and may not rate you higher for various health conditions.

Another significant pitfall of no medical exam plans is that there is going to be a strict limit on how much life insurance coverage you can buy. Most insurance companies will only allow you to get around $50,000 to $500,000 of life insurance without taking the exam.

Some applicants with Diabetes are going to need more coverage than that, which means that you’ll need to purchase more than one policy or apply for a traditional policy that requires further underwriting. Good news is, if you wanted to, you could take out multiple policies to address your financial concerns. When working with an agent from Diabetes Life Solutions, they will help you make the best decision for you and your family.

How to Save Money on Whole Life Insurance with Diabetes

While we can help you with the application process and determine what life insurance companies are ideal, we can’t help your overall health profile. What we can recommend is that you follow everything your doctor has suggested for your particular condition. Also, if you see an Endocrinologist, majority of life insurance companies will view you as a more favorable risk, compared to a person who does not.

People who are applying for a policy that requires a blood and urine test, should make sure their diabetes is under optimal control. If you go into your physical and your Glucose levels are all over the place, you can be pretty confident that your life insurance rates will be higher for your whole life insurance policy compared to a person who’s Diabetes levels are controlled.. Or if your medical records aren’t ideal, companies can decline you all together. Life insurance companies want to be sure that your diabetes is under control, and that you are compliant with your Doctor’s orders.

Most life insurance companies put an emphasis on your A1C levels. Ideally, they would like to see consistent readings of 7.5 or below. Before applying, and undergoing a blood test, it’s generally a good idea to speak with your Dr. office, and obtain the most recent readings. If your A1C is abnormally high, it’s probably a wise decision to postpone applying until you can lower your levels.

Every life insurance carrier is going to view A1C readings differently. One may rate you higher if your A1C is 7.3, where another carrier would not. This is why it’s important to work with agents who are properly trained to work with the Diabetes community. Here at Diabetes Life Solutions, we only work with people who have Diabetes, secure the best possible policy. Since we are considered an independent life insurance agent, we don’t just represent one or two companies. Rather we work with the best companies who will underwrite the diabetes community.

For some individuals with Diabetes, you may need to improve your overall health before applying. There are several ways that you can do that, like starting a diet and getting regular exercise. Both of these are going to help you manage your diabetes, lower your cholesterol, shed extra weight, lower your blood pressure, and much more. The healthier your lifestyle, the prettier picture you can paint to the life insurance company. Those with a healthy lifestyle can be rewarded with lower rates, compared to diabetics who are not in as good health.

All of these are going to translate into lower monthly premiums on your diabetes whole life insurance policy. Depending on your exact Height and Weight, losing 10 to 15 pounds may lead to lower premiums. If your Doctor has recommended any procedures, or referrals to specialists, you’ll need to complete these before applying for life insurance as well.

The next thing that you should do is eliminate any tobacco that you currently use. Smokers or chewing tobacco users are going to pay much more for their life insurance coverage versus what a non-smoker is going to pay. In fact, smokers pay almost twice as much for the same amount of life insurance protection. If you want to get the most affordable whole life insurance plan available, you’ll need to kick those bad habits once and for all. Also, if you do take out a policy as a tobacco user, and refrain from tobacco use for 12 months, you can always apply and receive a better priced policy, as a non-tobacco user.

If your diabetes condition is worsening, or you feel you don’t have a good chance of being approved for a fully underwritten policy, you might consider going for another type of whole life insurance altogether.

There are types of insurance such as Guaranteed Issue Life Insurance which can be expensive for people who are in average to above average health. But these policies are a great option for people who are in poor health, had a recent health issue or medical procedure, and can’t be approved for any other types of policies.

Guaranteed acceptance policies will offer coverage to anyone. No medical questions are asked. Since these policies are designed to cover people in poor health, and who may have Diabetes related complications ( Retinopathy, Neuropathy, etc.) they will not pay out the FULL DEATH BENEFIT until the policy is over two years old. Meaning if the insured were to pass away in first two years, the beneficiary would receive back all premiums paid, plus 10%. If death occurs at any point beyond the first two policy years, the beneficiary will receive the full amount of the policy.

Whole life insurance policies like these should be a last resort. When working with our agents, they will review your health profile, and let you know what whole life insurance plans you will qualify for. If you can qualify for a whole life insurance policy that offers an immediate death benefit pay out, we will direct you to those specific companies. Let us do all the hard work on your behalf!

Calculating Your Life Insurance Needs

Before you apply for any coverage, it’s vital that you get enough life insurance protection for your loved ones. When you’re determining what your insurance needs are, there are several factors that you should consider. Our agents are more than happy to assist, and to have a brief conversation with you to help determine the proper amount of life insurance.

Everybody’s financial objectives are different. Some people may need a whole life insurance designed to cover them up until retirement, and then possibly use the cash value of the policy as part of their retirement income. Others may only want to pay on a policy for twenty years, and then to cease making premium payments.

The first number to crunch is your debts and final expenses that you would leave behind to your family members. If something tragic were to happen to you, your loved ones could be left with a massive amount of debt, which can make an already difficult situation a thousand times worse. Many individuals may need $10,000 to $20,000 to cover various final expenses and funeral expenses.

The main goal of your life insurance is to give your family the money that they need to pay off those bills and unpaid costs. IN addition to burial expenses, there may be other type of debt. Cell phone bills, utility bills, credit card debt, or medical expense. Whole life insurance policies are designed to cover your entire life, and would pay a death benefit to your beneficiaries, to cover expenses like this.

The next number to look at is your salary. The secondary goal of your whole life insurance is to replace your paycheck if something tragic were to happen to you. If you’re one of the main providers in your house, your loved ones would suffer financially if you were to pass away. According to Dave Ramsey, you should have 10 times your salary in life insurance. While not everybody needs this amount of insurance, it does give you a starting point, to begin thinking about how much you need.

Your life insurance policy will give them the money that they need to pay for basic expenses without having to sacrifice their standard of living. By replacing your income your family can continue to live in their house, maintain current lifestyle, or provide enough money to put children thru college. Whole life insurance policies pay out a tax free death benefit, and your beneficiaries will have complete control of how to use these funds.

Final Thoughts

The most important thing to remember though, is that just because you have Diabetes, whole life insurance is definitely not out of reach for you. There is no reason that your family should have to go through life worrying about what will happen to them if something were to happen to you.

Stop thinking that you are unable to be insured and contact a trusted diabetes life insurance representative who can help to walk you through the process of getting yourself a policy you can actually afford.

We know that finding the perfect life insurance plan can be a long and difficult process, especially as a diabetic. Our agents can help you find the best plan to meet your needs at an affordable rate. Our goal is to make this process as simple as possible.

You never know what’s going to happen tomorrow, which means that you shouldn’t wait any longer to get the life insurance protection that your family deserves. There’s never a better time to start having discussions about your need for coverage.

Not having life insurance is one of the worst mistakes that you can make for your loved ones. If something tragic were to happen to you, you would leave your family with a massive mountain of debt and it will make an already difficult situation a thousand times worse.

Whole life insurance for diabetics is not difficult to obtain. This valuable type of life insurance could benefit you and your family some day. Do not think that having Diabetes disqualifies you from receiving an affordable life insurance policy.

Contact one of our agents today at 888-629-3064 and we can get the process started. The initial phone call takes 5 minutes or less. We love working with the diabetes community, as we are apart of the diabetes community. Do not hesitate to reach out to us and let our team help you and your family.